Crypto Exchange Restrictions for Iranian Citizens in 2025: What’s Blocked and How People Adapt

For Iranian citizens, using cryptocurrency isn’t about speculation anymore-it’s about survival. In 2025, the government has turned crypto from a tool of financial freedom into a tightly controlled, high-risk activity. While mining is still legal, buying, selling, or even holding digital assets has become a legal gray zone filled with sudden blackouts, frozen wallets, and strict time limits. If you’re an Iranian user trying to access crypto today, you’re not fighting against technology-you’re fighting against a state that wants to own every digital transaction.

Payment Gateways Shut Down, But Mining Still Allowed

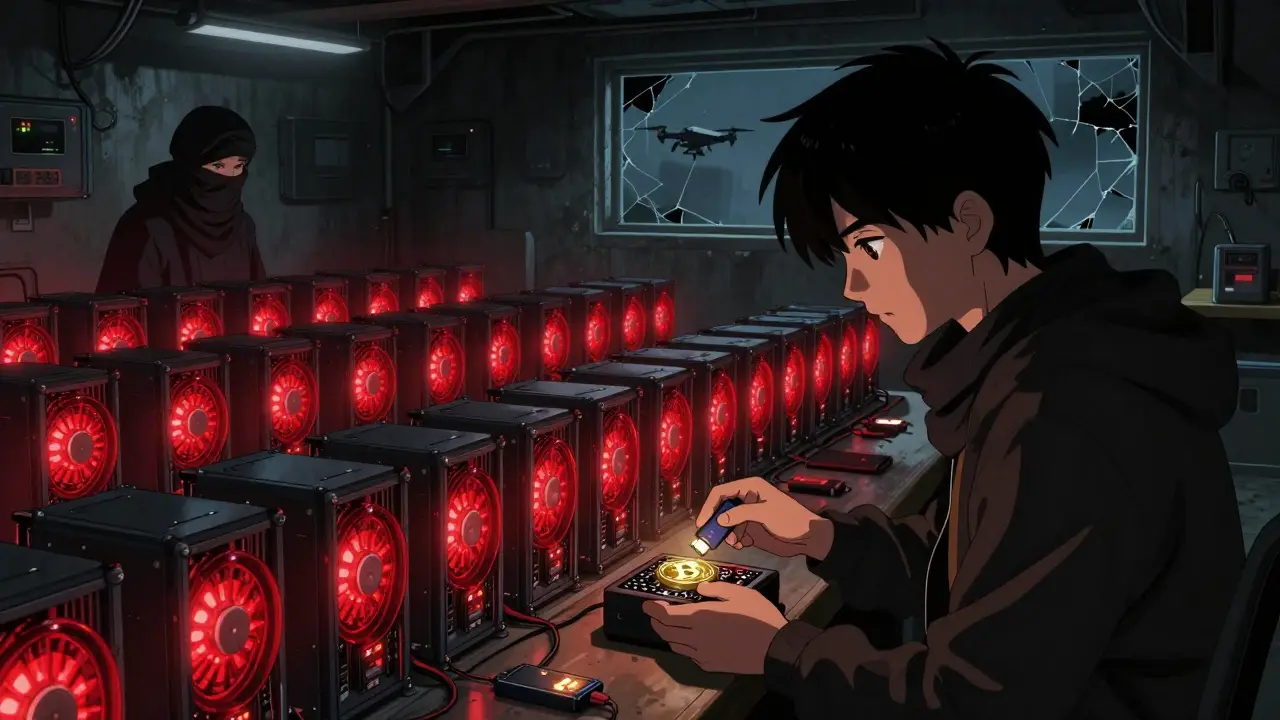

In January 2025, the Central Bank of Iran (CBI) pulled the plug on all rial payment channels for cryptocurrency exchanges. That meant no more bank transfers, no more digital wallets linked to local banks, no way to buy Bitcoin or Ethereum with Iranian rials through official channels. The move wasn’t about stopping crypto-it was about stopping uncontrolled crypto. The government estimated that exchanges had processed billions in transactions over the past two years without paying a single rial in taxes. Operators were operating in the shadows, and the state wanted them in the light-or out of the game entirely. Here’s the twist: cryptocurrency mining is still legal. Iran has one of the largest mining operations in the world, thanks to cheap electricity. The government doesn’t care if you’re using your home computer to mine Bitcoin. What they care about is what you do with it after. If you try to convert that mined Bitcoin into cash, pay for imports, or send it abroad, you’re now breaking the law.The Nobitex Hack That Changed Everything

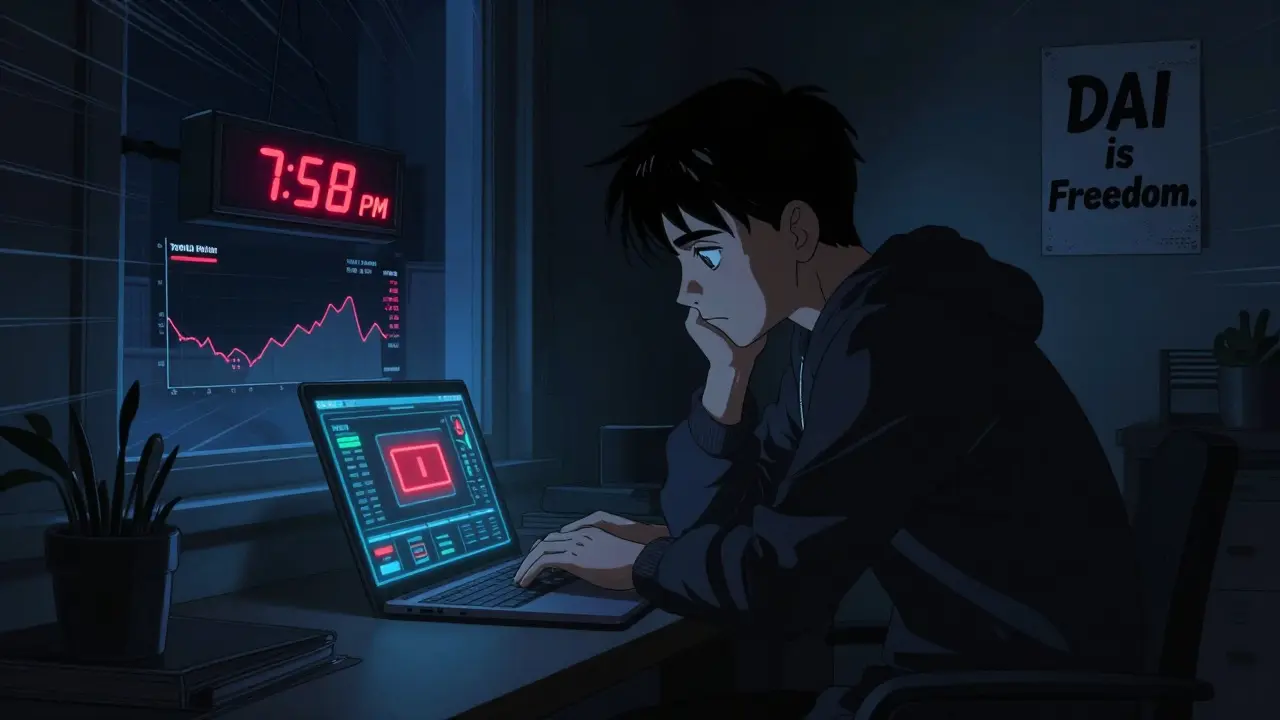

On June 18, 2025, Nobitex-Iran’s biggest crypto exchange with over 11 million users-was hacked. Attackers drained more than $90 million in assets. The breach wasn’t just a technical failure; it was a political earthquake. Within hours, the CBI responded with a radical new rule: all domestic exchanges must shut down between 8:00 PM and 10:00 AM local time. These hours weren’t chosen randomly. They were designed to make trading nearly impossible for average users. Most Iranians work 9-to-5 jobs. By the time they get home, the market is already closed. The few who can trade during the 10 AM to 8 PM window face overcrowded platforms, slow confirmations, and massive price swings. The result? Trading volume dropped by 40% in the weeks after the restriction. Tether (USDT), the stablecoin Iranians relied on to protect their savings from inflation, spiked to over 12,000 Toman on local exchanges-up from 10,500 just days before. People panicked. They knew the government was watching, and they feared more freezes were coming.Tether Freezes $90 Million in Iranian Wallets

On July 2, 2025, Tether-the company behind USDT-froze 42 cryptocurrency addresses linked to Nobitex. This wasn’t a random action. The frozen wallets showed clear transaction trails connecting to addresses previously flagged by Israeli counter-terrorism agencies as tied to Iran’s Islamic Revolutionary Guard Corps (IRGC). Tether didn’t accuse ordinary users. They targeted wallets with patterns of large, irregular transfers, often moving funds through multiple layers to obscure origins. For everyday Iranians, this was devastating. Many had stored their life savings in USDT because it was stable, fast, and widely accepted. Overnight, thousands lost access to funds they’d used to pay rent, buy medicine, or send money to family abroad. Some had deposited their money through third-party OTC traders who claimed to be “safe.” Now those traders vanished. The message was clear: if you’re using crypto in Iran, you’re not just at risk from hackers-you’re at risk from global financial enforcers.

Iran’s First Crypto Tax Law: Pay Up or Get Caught

In August 2025, Iran passed its first-ever law taxing cryptocurrency profits. The Law on Taxation of Speculation and Profiteering treated crypto gains the same way it treats gold, real estate, or forex trading. If you made a profit selling Bitcoin or swapping USDT for Ethereum, you now owe taxes. The tax rate? 15% on net gains, with penalties for underreporting. The government didn’t just want money-they wanted visibility. Before this law, crypto trades were invisible to tax authorities. Now, exchanges are required to report user transactions to the Iranian Tax Organization. If you’re trading on an unlicensed platform, you’re not just breaking financial rules-you’re risking criminal charges. The law’s rollout was slow and uneven. The first phase targeted only licensed exchanges. The second phase, expected in early 2026, will require wallet providers to integrate reporting tools. This means even if you hold crypto in a personal wallet, you’ll soon be forced to declare your holdings-or risk audits, fines, or worse.U.S. Sanctions Hit Iran’s Crypto Shadow Network

The U.S. didn’t sit back while Iran tightened its own rules. In September 2025, the Treasury Department’s Office of Foreign Assets Control (OFAC) sanctioned a $600 million shadow banking network linked to Iran’s military. The network used crypto to launder over $100 million in oil profits through front companies in Turkey, the UAE, and Malaysia. The key player? Arash Estaki Alivand, a financial facilitator whose Ethereum and Tron wallets were directly tied to the scheme. OFAC froze 89 addresses linked to him. Many of these wallets had previously interacted with Iranian exchanges like Nobitex and Binance Iran. This move didn’t just hurt state actors-it hurt ordinary users. Binance, which had quietly allowed Iranian users to trade through peer-to-peer (P2P) channels, suddenly pulled out of Iran entirely. Other platforms followed. The result? Iranian users lost access to the last reliable global gateways. P2P trading became riskier than ever. Buyers and sellers now fear being flagged by automated compliance systems that scan for Iranian IP addresses or transaction patterns.

Jordan Fowles

December 27, 2025 AT 01:07The resilience of ordinary Iranians in the face of systemic suppression is one of the most profound examples of human adaptability in the digital age. This isn't just about crypto-it's about the right to economic dignity when institutional systems fail. The state's attempt to control access by restricting trading hours and freezing stablecoins reveals a fundamental misunderstanding: you cannot suppress a need, only redirect it. What we're seeing isn't a decline in usage-it's an evolution into more decentralized, resilient forms. DAI, burner wallets, Telegram-based OTC, cross-border flash drives-these aren't hacks. They're civil society building its own financial infrastructure from the ground up.

And yet, the global response has been chillingly predictable: sanctions that punish the vulnerable, corporate compliance that erases entire user bases, and the moral surrender of platforms like Binance. The irony is thick-crypto was supposed to liberate, but now it's the tool of the powerful to isolate the powerless. The real revolution isn't in the blockchain. It's in the people who refuse to be erased.

History will remember this not as a regulatory crackdown, but as the moment financial sovereignty became a human rights issue.

Adam Hull

December 28, 2025 AT 23:28Let’s be honest-this entire narrative is just performative victimhood wrapped in blockchain jargon. The Iranian government isn’t the villain here; it’s the only entity trying to prevent a full-scale financial collapse fueled by unregulated speculation. The fact that people are using crypto to bypass sanctions doesn’t make them heroes-it makes them enablers of state-sponsored criminal networks. Tether froze those wallets because they had clear IRGC links. That’s not oppression, that’s compliance. And now you want us to feel bad because ordinary people got caught in the crossfire? Newsflash: if you choose to operate in a sanctioned economy, you accept the consequences.

DAI? Really? You think decentralization saves you when every node is monitored? The real tragedy isn’t the freezes-it’s that people still believe technology can outsmart geopolitics.

Mandy McDonald Hodge

December 30, 2025 AT 02:38i just cried reading this. like… how do you even sleep at night knowing your savings could vanish because someone in a different country flagged your wallet? i’ve never used crypto but now i feel like i understand why people risk everything for it. it’s not about getting rich-it’s about not starving. and the fact that we’re talking about ‘trading windows’ like it’s a stock market session… that’s just heartbreaking. please don’t call it ‘speculation’-it’s survival.

also dais are the real MVPs. someone pls make a tshirt that says ‘i hold dai because the world froze my life savings’ 😭

Willis Shane

December 31, 2025 AT 20:18Adam Hull's comment is a textbook example of Western moral grandstanding disguised as empathy. The notion that Iranians are ‘building financial infrastructure’ is not only naive-it’s dangerously ignorant. This isn’t civil society; it’s an underground economy that funnels billions into the coffers of the IRGC. The fact that you romanticize DAI usage while ignoring the documented links between these wallets and terror financing reveals a profound ethical blindness. This isn’t about human rights-it’s about enabling state-sponsored sanctions evasion. And no, the people aren’t ‘rewriting the rules’-they’re just becoming more sophisticated criminals.

Let me be clear: if you support crypto access in Iran without demanding full transparency and accountability for fund origins, you’re complicit.

Andrew Prince

January 1, 2026 AT 07:17It is, in fact, a fascinating case study in the paradox of technological emancipation within authoritarian frameworks. The state, in its attempt to exert control over digital financial flows, inadvertently catalyzes the very decentralization it seeks to suppress. The imposition of trading curfews, the freezing of stablecoin assets, and the criminalization of unlicensed exchanges have collectively produced a decentralized, peer-to-peer, community-driven financial ecosystem that operates outside the purview of both the Iranian state and Western regulatory bodies. This is not merely adaptation-it is emergent governance.

Moreover, the selective enforcement of sanctions by OFAC, which targets not only IRGC-linked entities but also incidental users through IP-based de-anonymization protocols, demonstrates the inherent contradiction of global financial hegemony: the same institutions that preach financial inclusion and open access simultaneously engineer exclusionary architectures that disproportionately impact the most vulnerable. The result is a bifurcated digital economy-one for the sanctioned, one for the sanctioned-against.

One must ask: if the global financial system is so committed to transparency, why does it remain blind to the suffering it enables? The answer lies not in technology, but in power.

prashant choudhari

January 2, 2026 AT 12:31Real talk. Mining is legal because it uses electricity the government sells cheap. But if you try to turn that Bitcoin into food or medicine? You're a criminal. That's not regulation. That's theft by bureaucracy.

People are using DAI because it's the only thing that can't be turned off by a single company. Tether froze wallets? Fine. But they didn't freeze the network. The network still runs.

This isn't about crypto. It's about who gets to decide if you live or starve. And right now, Tehran and Wall Street are both making that call.

Steve Williams

January 3, 2026 AT 20:55As someone from Nigeria, I recognize this struggle intimately. Our own government has attempted similar restrictions on crypto under the guise of financial control, yet millions still find ways to use it. The resilience of people in Iran reminds me of what we’ve seen in Lagos and Abuja-when formal systems fail, communities build their own. What’s happening isn’t illegal-it’s inevitable.

It’s important to note that the global response has been too slow. Sanctions that freeze wallets don’t punish the regime-they punish mothers, students, and small business owners. The world needs to distinguish between state actors and civilians. Crypto isn’t the enemy. The lack of humane policy is.

Let us not mistake survival for sin.

Jake West

January 5, 2026 AT 06:04Wow. So the solution to state oppression is… using a different stablecoin? That’s it? You’re telling me people are risking jail time to swap USDT for DAI because… it’s decentralized? Bro. You’re not a revolutionary. You’re just using a slightly less traceable app.

And don’t even get me started on ‘burner wallets’ and ‘Telegram groups’. That’s not innovation-that’s a 2014 Bitcoin forum thread with a VPN. The fact that you’re treating this like some underground hacker movement is just cringe. Most of these people just want to buy groceries without their life savings vanishing overnight.

Stop romanticizing desperation. It’s not edgy. It’s tragic.