How Crypto Exchanges Implement AML to Stop Money Laundering

When you buy Bitcoin or trade Ethereum on a crypto exchange, you might think it’s just a simple swap of digital coins. But behind the scenes, there’s a whole system working to make sure that money from drug deals, scams, or ransomware isn’t getting cleaned and turned into "legit" crypto. This is called AML - anti-money laundering - and it’s not optional anymore. Since 2019, crypto exchanges have been legally required to treat users like banks do: verify identities, track every dollar, and report anything suspicious. Failure? You could face $100 million in fines - or jail time for founders.

Why AML Matters More Than Ever in Crypto

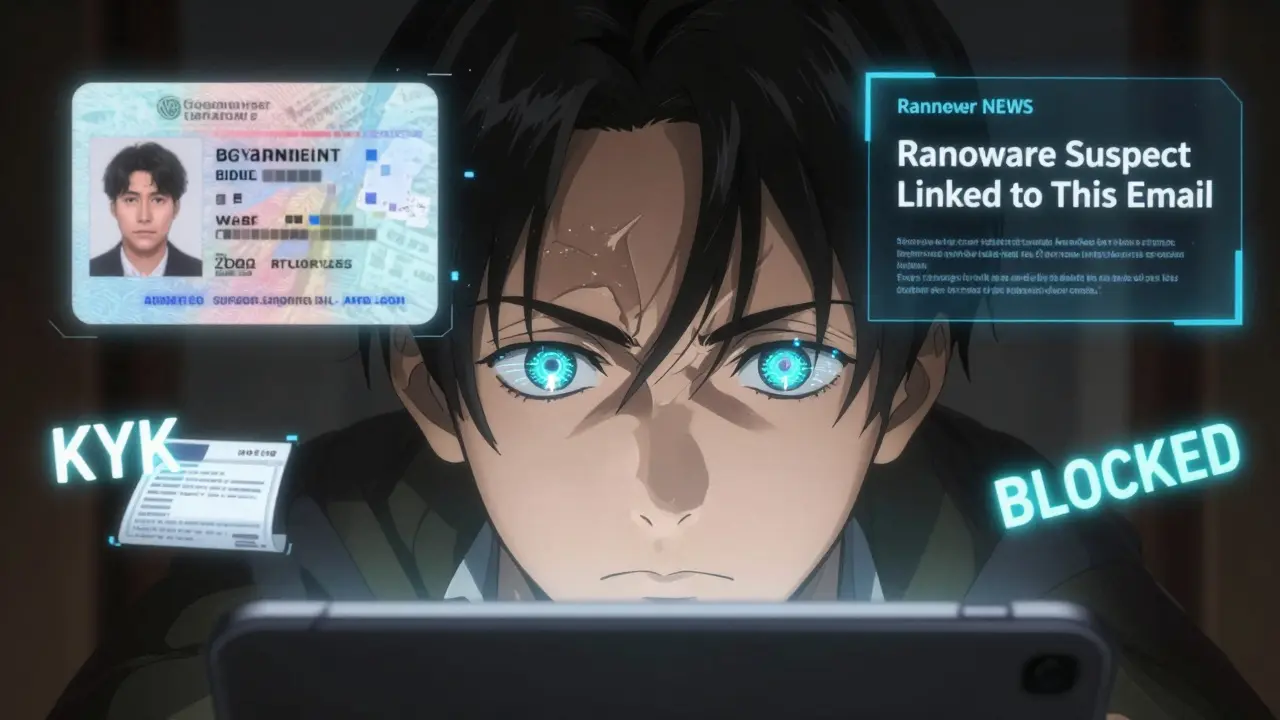

Cryptocurrencies were built on anonymity. Bitcoin transactions don’t show names - just wallet addresses. That made them attractive to criminals. But as crypto grew, regulators couldn’t ignore it. In 2019, U.S. agencies like FinCEN, the SEC, and CFTC made it official: crypto exchanges are financial institutions. That meant they had to follow the same rules as banks under the Bank Secrecy Act. The same law that stops drug cartels from depositing cash in bank accounts now stops them from converting stolen Bitcoin into stablecoins or fiat currency. The global standard comes from the Financial Action Task Force (FATF), an international body that sets rules to fight financial crime. They gave crypto exchanges three core tasks: Know Your Customer (KYC), monitor transactions, and respond when something looks off. No more hiding behind "we’re just a tech platform." If you run a crypto exchange today, you’re a financial gatekeeper.Know Your Customer: The First Line of Defense

Before you can trade on most major exchanges, you have to prove who you are. This isn’t just uploading a selfie - it’s a full identity check. You’ll typically need:- A government-issued ID (passport, driver’s license)

- A proof of address (utility bill, bank statement)

- A live video selfie or facial scan to match your ID

Transaction Monitoring: Watching Every Move

KYC is just the start. Once you’re in, the system watches every transaction. Not just the big ones - all of them. A $50 transfer from your wallet to another wallet might seem harmless. But if that same wallet has received funds from a known darknet marketplace, or if you’re sending $50 every 20 minutes to 50 different addresses, the system picks it up. There are three main ways exchanges monitor transactions:- Deny Lists: Block transactions from or to wallets linked to past crimes - like the Lazarus Group (North Korean hackers) or Silk Road addresses. This is the most common approach.

- Allow Lists: Only allow transactions between wallets that have passed full KYC. This is stricter and rare in public exchanges, but used by some institutional platforms.

- Pattern Recognition: AI analyzes behavior over time. If you usually trade $1,000 every Friday, then suddenly send $50,000 to a new wallet in a high-risk country? That’s flagged. If you’re sending small amounts to multiple wallets to avoid detection - called "structuring" - the system spots it.

How Exchanges Respond When Something’s Wrong

Finding a red flag isn’t enough. You have to act. When an exchange’s system detects suspicious behavior, it triggers a response protocol:- Immediate account freeze or transaction hold

- Internal review by compliance team

- Contact with the user for clarification (e.g., "Why are you sending this to a wallet in Iran?")

- Updating user risk profile - maybe now they’re "high risk"

- Filing a Suspicious Activity Report (SAR) with financial authorities

The Global Patchwork of Rules

You can’t just follow one set of rules. If your exchange operates in the U.S., EU, Singapore, and Japan, you’re juggling four different legal systems.- In the U.S., the Bank Secrecy Act requires SARs, KYC, and recordkeeping for 5 years.

- The EU’s 5AMLD requires exchanges to verify all customers, even those using peer-to-peer platforms.

- Japan requires exchanges to register with the Financial Services Agency and submit quarterly compliance reports.

- Switzerland allows more flexibility but demands rigorous internal audits.

Technology Behind the Scenes

You don’t hire 100 people to manually check transactions. That’s impossible at scale. Instead, exchanges use:- AI-driven risk scoring: Each user gets a risk score based on location, transaction history, wallet behavior, and more. High score? Extra checks.

- Dynamic APIs: Connect to real-time sanctions databases, PEP lists, and blockchain analytics tools.

- Low-code platforms: Compliance teams can update rules without waiting for engineers - like changing a filter to block all transactions to wallets created after January 1, 2025.

- Biometric authentication: Facial recognition, voice patterns, even typing speed to detect impersonation.

What Happens When You Fail

The penalties aren’t theoretical. In 2021, a derivatives exchange paid $100 million to settle AML violations. In 2022, three founders of a crypto startup pleaded guilty to violating the Bank Secrecy Act. Each paid $10 million in fines and faced prison time. One got 18 months. These aren’t outliers. They’re warnings. Regulators are watching. And they’re getting smarter. In 2025, the U.S. Treasury announced new rules requiring crypto exchanges to report transactions over $10,000 - just like banks. That’s coming to more countries soon.The Balance: Security vs. User Experience

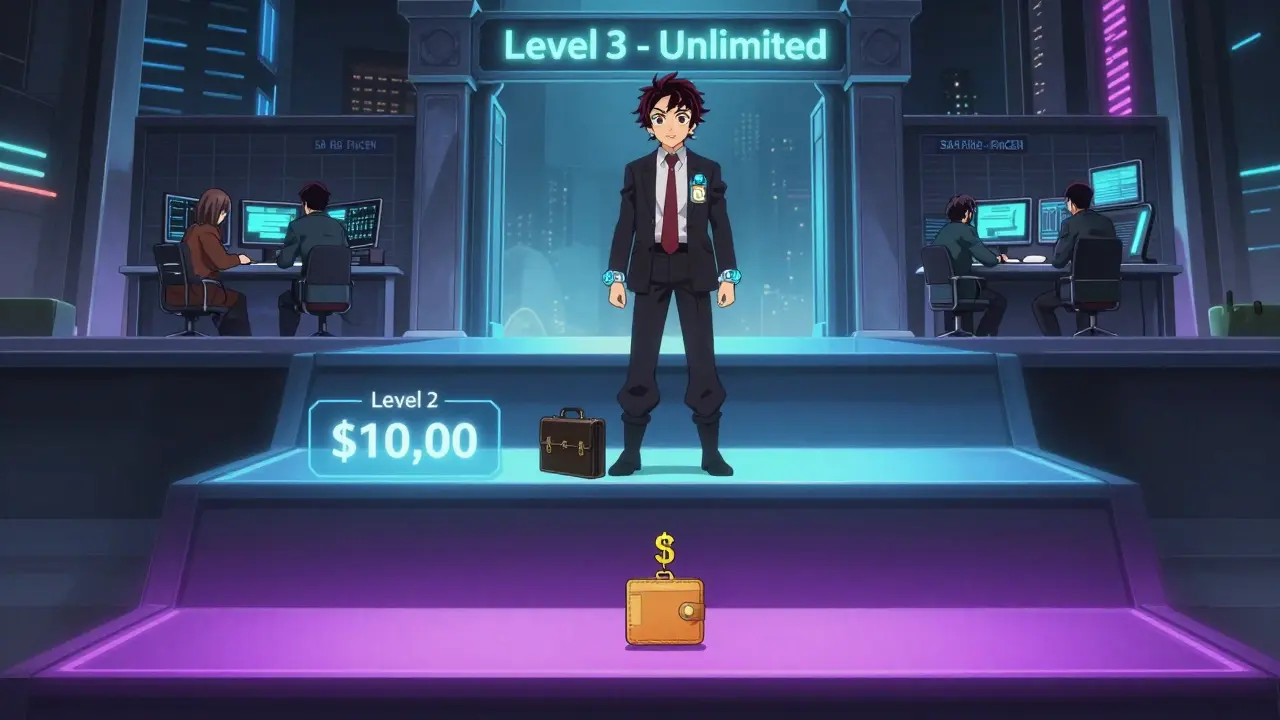

The hardest part? Making AML work without driving users away. Too many verification steps? People leave. Too little? You get fined. The best exchanges find the middle ground. Some offer tiered access:- Level 1: No KYC - can only deposit $100/month, no withdrawals

- Level 2: Basic ID - $10,000/month limit

- Level 3: Full KYC + biometrics - unlimited trading

What’s Next for AML in Crypto

The next wave is decentralized finance (DeFi) and peer-to-peer trading. Right now, most AML rules apply only to centralized exchanges. But regulators are pushing to extend them to DeFi protocols and even wallet providers. The FATF is already drafting guidelines for "VASPs" - Virtual Asset Service Providers - that could include decentralized apps. That means in the next two years, you might need KYC just to use a non-custodial wallet that connects to a DeFi protocol. It’s controversial. But the trend is clear: no more anonymity loopholes. The future of crypto isn’t about being untraceable. It’s about being trustworthy. Exchanges that build strong, smart AML systems won’t just survive regulation - they’ll win user trust. And that’s the real edge in 2026.Do all crypto exchanges have to follow AML rules?

Yes - if they’re centralized and operate in regulated jurisdictions like the U.S., EU, UK, Japan, or Australia. Any exchange that converts crypto to fiat or offers trading services must comply. Decentralized exchanges (DEXs) without a central operator currently fall in a gray area, but regulators are moving to close that gap.

Can I avoid KYC on crypto exchanges?

Some smaller or offshore platforms claim to skip KYC, but they’re risky. You won’t be able to cash out to a bank account, and your funds could be frozen at any time. Even if you can trade, most major wallets and payment processors now block crypto from unverified sources. Avoiding KYC doesn’t make you safer - it makes your crypto useless.

Why do I need to take a selfie for crypto exchanges?

It’s called liveness detection. The system checks that you’re a real person, not a photo or deepfake. Criminals often use stolen IDs or synthetic identities. A live selfie with head movement or blinking proves you’re there - and helps prevent fraud before it starts.

What happens if my transaction gets flagged?

Your account will be temporarily frozen. The exchange’s compliance team will contact you to ask for details - like why you sent money to that wallet, or where the funds came from. If you provide clear, honest answers, your account will usually be unfrozen within 1-5 days. Refusing to answer or giving false info can lead to permanent closure and a report to authorities.

Is crypto really anonymous if exchanges do KYC?

No - not anymore. While blockchain transactions are public, your identity is now tied to your wallet through KYC. Once you use a regulated exchange, your crypto activity is no longer anonymous. The blockchain shows where coins go - and the exchange knows who you are. That’s the trade-off for legal, secure access to crypto markets.

Tiffani Frey

January 5, 2026 AT 17:20It’s fascinating how much infrastructure is hidden behind something that feels so simple-like buying BTC. I’ve used exchanges for years, but I never realized how many layers of verification, AI monitoring, and international compliance frameworks are actively working to prevent misuse. It’s not just about law enforcement; it’s about preserving the integrity of the entire ecosystem. If crypto wants to be taken seriously as a financial asset, this level of rigor isn’t optional-it’s foundational.

Ritu Singh

January 6, 2026 AT 12:51Surendra Chopde

January 6, 2026 AT 20:13Interesting breakdown. One thing missing is how KYC impacts users in developing countries-like in India-where government IDs are often outdated or inconsistently issued. Many legitimate users get flagged not because they’re suspicious, but because their documents don’t match the rigid formats Western systems expect. It’s not just about tech-it’s about cultural and institutional bias baked into compliance design.

Jennah Grant

January 8, 2026 AT 04:33There’s a critical tension here between regulatory compliance and financial inclusion. While AML protocols are necessary, the over-reliance on centralized identity verification excludes millions who lack formal documentation-refugees, undocumented workers, rural populations. True innovation would be developing decentralized, privacy-preserving identity solutions that satisfy regulators without excluding the vulnerable. We’re not there yet.

Becky Chenier

January 8, 2026 AT 19:43Veronica Mead

January 10, 2026 AT 00:31It is regrettably evident that the proliferation of unregulated digital asset platforms has enabled the systematic laundering of illicit capital on an unprecedented scale. The implementation of KYC and transaction monitoring protocols, while burdensome, is not merely advisable-it is an ethical imperative. Failure to comply constitutes a moral dereliction of duty to the global financial system. One must ask: if one has nothing to hide, why resist transparency?

Rahul Sharma

January 10, 2026 AT 15:02Good points. But let’s be real-most small exchanges in India or Africa just can’t afford Chainalysis or AI tools. They use basic lists and hope for the best. So yes, big exchanges are locked down, but the real risk is now shifting to unregulated platforms. That’s where the money still flows. Regulation needs to be smart-not just heavy-handed.

Paul Johnson

January 12, 2026 AT 14:07