Is Crypto Regulated in India? Tax Rules, Legal Status, and What You Need to Know in 2026

Is crypto regulated in India? The short answer: yes-but not the way most people expect. You can buy, sell, and hold Bitcoin, Ethereum, or any other cryptocurrency legally in India. But you can't use it to pay for groceries, and the government is watching every transaction closely. There's no outright ban, but there's also no official approval. Instead, India has built a system that treats crypto not as money, not as securities, but as a taxable digital asset-and that changes everything.

What Does "Regulated" Actually Mean in India?

In most countries, regulation means clear rules: who can operate, how they must protect users, and what rights buyers have. In India, regulation means taxes, tracking, and paperwork. Since August 2025, the Virtual Digital Assets (VDAs) are defined under Section 2(47A) of the Income Tax Act, 1961, as amended by the Income Tax (No. 2) Bill, 2025, and include all cryptocurrencies, NFTs, and other crypto tokens except Indian rupees are officially recognized as taxable property. That’s it. No license required to trade. No approval needed to hold. Just pay up-or risk penalties.Here’s what that looks like in practice:

- You can’t use Bitcoin to buy a phone at a store. It’s not legal tender.

- You can’t open a crypto savings account with a bank. RBI doesn’t allow it.

- You can’t claim losses on crypto trades to reduce your tax bill. Every gain is taxed at 30%, no deductions.

- You must pay 1% TDS on every trade, whether you made money or not.

This isn’t a gray area anymore-it’s a red line. The government doesn’t want crypto to replace rupees. It wants to tax it like gold or real estate.

The 30% Tax and 1% TDS: How It Works

Let’s say you bought 0.5 BTC for ₹15 lakh in 2023 and sold it in January 2026 for ₹28 lakh. Your profit? ₹13 lakh. Under Indian law, that entire ₹13 lakh is taxed at 30%. That’s ₹3.9 lakh in taxes. On top of that, the exchange you used automatically deducted ₹28,000 as TDS (1% of the sale value). That money goes straight to the government. You don’t get it back. Even if you lost money on other trades, you can’t offset it. Losses? Irrelevant.Here’s the kicker: TDS applies to every single transaction. Buy ETH? 1% TDS. Sell Solana? 1% TDS. Transfer crypto to a friend? 1% TDS. Even if it’s a gift. Even if it’s a swap. The system is designed to capture every movement. The Financial Intelligence Unit India (FIU-IND) is responsible for monitoring suspicious transactions and enforcing AML rules across all crypto exchanges operating in India tracks every transfer, and the Income Tax Department uses data from exchanges and blockchain analytics tools to match unreported crypto income cross-checks your bank statements, UPI logs, and exchange reports to find missing filings.

Many traders think they’re safe if they use foreign exchanges. They’re wrong. If you’re an Indian resident, the government still taxes your global crypto income. The 2025 tax law explicitly covers all residents, regardless of where the trade happened.

Who’s Watching You?

India doesn’t have one crypto regulator. It has five-and they’re all watching.- Income Tax Department Enforces the 30% tax on VDA gains and audits crypto traders using data from exchanges and blockchain analysis

- Financial Intelligence Unit India (FIU-IND) Monitors crypto platforms for money laundering, requiring KYC and transaction reporting

- Reserve Bank of India (RBI) Still opposes crypto as a payment method and is developing its own digital rupee

- Securities and Exchange Board of India (SEBI) Has proposed regulating crypto trading like stock markets, suggesting future oversight

- Ministry of Finance Sets the tax policy and is responsible for drafting future crypto legislation

Each agency has a different agenda. RBI fears crypto will destabilize the banking system. SEBI wants to bring it under market rules. The Finance Ministry just wants to collect tax. The result? A patchwork of rules that confuse users but make enforcement easier.

The History: From Ban to Tax

Back in 2018, the RBI didn’t just regulate crypto-it banned it. Banks were ordered to stop serving crypto exchanges. Thousands of startups shut down. Investors panicked. The industry thought it was over. Then came March 4, 2020. The Supreme Court ruled the RBI’s ban illegal. It was a win. Exchanges reopened. Trading surged. But the government didn’t give up. It just changed tactics. In 2019, tax notices started appearing. People who traded crypto got letters asking for transaction records, profit calculations, and proof of tax payment. The message was clear: we know what you’re doing. Pay up. By 2022, the government introduced a 30% tax on crypto gains. No one knew if it would stick. But in 2025, the Income Tax (No. 2) Bill, 2025 was passed with presidential assent, formally embedding the VDA tax regime into Indian law. This wasn’t a temporary rule. It was a permanent shift.What’s Still Unclear?

Despite the tax law, big questions remain unanswered:- Can you mine crypto in India? No official rules yet.

- Is staking taxable? Yes, but how? Is it income or capital gain?

- What about DeFi? Lending, borrowing, yield farming? The government hasn’t said.

- Can you inherit crypto? How is it valued? No clear guidance.

- Will NFTs be taxed differently than Bitcoin? Not yet.

These gaps aren’t accidents. They’re intentional. The government is waiting to see how global rules evolve before locking in specifics. Meanwhile, Indian traders are left guessing.

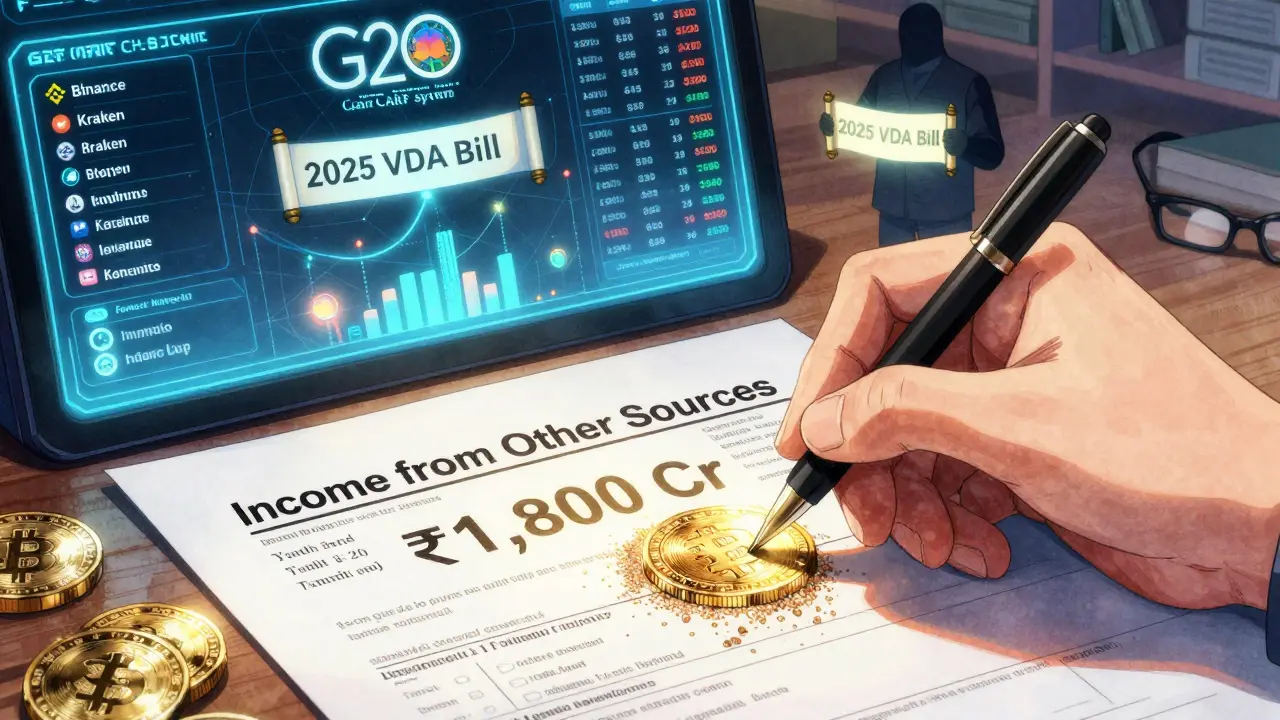

Global Pressure and the G20 Effect

India didn’t create this tax system in a vacuum. In 2023, at the G20 summit, India pushed for global standards on crypto reporting. The result? The Crypto-Asset Reporting Framework (CARF), which will force exchanges worldwide to share data with Indian tax authorities starting in 2027. That means even if you trade on Binance or Kraken, the Indian government will eventually know.It’s not about stopping crypto. It’s about controlling it. By aligning with international standards, India ensures it won’t be left behind as a tax haven for crypto profits. It’s also a warning: if you don’t report, someone else will.

What Should You Do Now?

If you hold or trade crypto in India, here’s what you need to do:- Track every transaction: buys, sells, swaps, gifts, staking rewards.

- Keep records of purchase price, date, and exchange used.

- Pay 1% TDS on every trade-it’s automatic, but you still need to account for it.

- Report all crypto gains under "Income from Other Sources" in your tax return.

- Don’t assume foreign exchanges are safe. The government is already preparing to collect data.

There’s no way around the tax. But if you stay organized, you can avoid penalties, notices, and audits. The government isn’t trying to scare people away-it’s trying to collect revenue. Be ready.

What’s Next?

The next big step? A formal crypto law. The draft bill from 2019, which aimed to ban private crypto and launch a digital rupee, is still sitting on the table. Experts expect a new version to be introduced in 2026. It might allow regulated exchanges. It might require licensing. It might even let banks partner with crypto firms.But one thing won’t change: the 30% tax. That’s here to stay. The government has made too much money from it. In the 2024-2025 fiscal year, crypto taxes brought in over ₹1,800 crore. That’s more than what India earned from gold imports. Why would they give that up?

India’s approach isn’t unique. Countries like the UK, Australia, and Japan also tax crypto as property. But India’s 30% rate and 1% TDS are among the strictest in the world. You won’t find a country that taxes every single transaction like this.

So yes, crypto is regulated in India. Just not how you thought.

Is it legal to buy Bitcoin in India?

Yes, it is legal to buy, sell, and hold Bitcoin and other cryptocurrencies in India. There is no ban on owning or trading crypto. However, it is not recognized as legal tender, meaning you cannot use it to pay for goods or services in regular stores or businesses. All transactions are subject to tax and reporting rules under the Virtual Digital Assets (VDA) framework.

Do I have to pay tax on crypto even if I didn’t sell?

Yes. Under India’s 2025 tax rules, any transfer of a Virtual Digital Asset (VDA)-including swapping one crypto for another, gifting crypto, or using it to buy something-is considered a taxable event. Even if you didn’t convert to rupees, you still owe 30% tax on the gain and 1% TDS on the transaction value. Holding alone isn’t taxed, but any movement of assets triggers tax.

Can I offset crypto losses against gains?

No. Unlike stocks or mutual funds, you cannot use losses from crypto trades to reduce your taxable gains. If you lost ₹5 lakh on Ethereum but made ₹8 lakh on Bitcoin, you still pay 30% tax on the full ₹8 lakh. Losses cannot be carried forward or deducted. This is one of the strictest aspects of India’s crypto tax law.

What happens if I don’t report my crypto income?

If you don’t report crypto income, the Income Tax Department can issue a notice demanding payment of unpaid taxes, interest, and penalties. The department already receives transaction data from Indian exchanges and is preparing to collect data from global platforms under the G20’s CARF system. Non-compliance can lead to penalties of up to 200% of the tax due, and in extreme cases, prosecution under the Income Tax Act.

Will the government ban crypto in the future?

A full ban is unlikely. The government has moved from prohibition to taxation, and the tax revenue from crypto is significant-over ₹1,800 crore in 2024-2025. While a new law may introduce licensing or stricter rules for exchanges, outright banning crypto would mean losing a major source of tax income. The trend is toward control, not elimination.

Are NFTs treated the same as Bitcoin in India?

Yes. Under the 2025 VDA tax law, NFTs are explicitly included in the definition of Virtual Digital Assets. Any sale, transfer, or exchange of an NFT is subject to the same 30% tax rate and 1% TDS as Bitcoin or Ethereum. Whether it’s a digital artwork, game item, or collectible, if it’s a token on a blockchain, it’s taxed the same way.

Can I use a foreign crypto exchange to avoid taxes?

No. Indian tax law applies to all residents, regardless of where they trade. If you’re an Indian citizen or resident, your global crypto income is taxable in India. The government is already working with international partners under the G20’s CARF framework to collect transaction data from foreign exchanges. Hiding trades overseas won’t protect you-it just makes detection easier.

Is mining cryptocurrency legal in India?

Mining is not explicitly banned, but it’s not officially regulated either. Any income from mining-such as newly minted Bitcoin or Ethereum-is considered taxable under "Income from Other Sources" at 30%. You must report the fair market value of the coins when received. There are no specific rules for electricity usage, equipment, or mining pools, so miners operate in a legal gray zone.

rajan gupta

March 16, 2026 AT 03:51Billy Karna

March 16, 2026 AT 13:55Arlene Miles

March 16, 2026 AT 23:16Jessica Beadle

March 17, 2026 AT 04:18Tony Weaver

March 18, 2026 AT 22:12Patty Atima

March 19, 2026 AT 10:30Lucy de Gruchy

March 20, 2026 AT 10:03Tobias Wriedt

March 20, 2026 AT 11:06iam jacob

March 20, 2026 AT 20:39Jesse Pals

March 22, 2026 AT 17:19